NAPC Defense – Contracting and Defense Operations

Strategic Overview

NAPC Defense, Inc. is a U.S.-licensed defense manufacturer and public company that serves as the primary subcontractor and principal public-company execution platform for major U.S. government contract work performed in partnership with Native American Pride Constructors, LLC. The company also maintains broader defense and law-enforcement business lines, including weapons systems, munitions, tactical equipment, ballistic protection, armored solutions, and exclusive rights to produce and distribute the CornerShot USA system.

NAPC Defense, Inc. is a U.S.-licensed defense manufacturer and public company that serves as the primary subcontractor and principal public-company execution platform for major U.S. government contract work performed in partnership with Native American Pride Constructors, LLC. The company also maintains broader defense and law-enforcement business lines, including weapons systems, munitions, tactical equipment, ballistic protection, armored solutions, and exclusive rights to produce and distribute the CornerShot USA system.

NAPC Defense’s status has materially changed. The company now stands at the center of an operating government-contracting platform with hard backlog, multi‑billion‑dollar IDIQ access, integrated personnel, an agreed $20 million operational credit line, active contract payments and bid activity, and a growing defense-products business under the CornerShot and munitions platforms.

Obera Acquisition, Government Novation, and Approval

Native American Pride Constructors did not simply receive contract novations from Obera LLC. It acquired Obera, and only after that acquisition did the relevant government contracts undergo formal novation and approval by the appropriate Department of Defense contracting officers.

As part of that process, the Government’s review addressed, among other things:

Native American Pride Constructors’ ability to assume and continue contract performance.

Continuity of personnel, capabilities, and management between Obera and the successor structure.

Whether transfer of the contracts from Obera to Native American Pride Constructors was in the best interest of the United States Government.

In parallel, NAPC Defense was also reviewed and accepted by the contracting officers and the Department of Defense as the primary subcontractor and principal public-company platform responsible for executing the bulk of subcontracted work on these lines. In other words, both Native American Pride Constructors, as successor prime, and NAPC Defense, as main subcontractor, were passed upon and found acceptable for their respective roles in continuing performance under the contracts.

The outcome of this combined review and novation process is a formal determination that:

Native American Pride Constructors is an approved successor in interest to Obera on the affected contracts.

NAPC Defense is an acceptable primary subcontractor and execution platform for the work to be performed under these vehicles.

This constitutes a meaningful “stamp of approval” by the U.S. Government on the Native American Pride Constructors / NAPC Defense platform.

Novated IDIQ Portfolio and Backlog

The Obera portfolio, now under Native American Pride Constructors with NAPC Defense as the primary subcontractor, includes:

Approximately $38.1 million in existing U.S. government task orders (hard backlog) running into 2027.

Approximately $57.1 billion in combined IDIQ ceilings, consisting of:

U.S. Navy Counter Narcotics and Global Threats (CNGT) IDIQ with an approximate $1.9 billion ceiling.

U.S. Air Force Worldwide Expeditionary Multiple Award Contract (WEXMAC) IDIQ with an approximate $55.2 billion ceiling.

These positions give NAPC Defense an ongoing foothold in substantial, long-duration contract vehicles that are central to current Department of Defense mission-support and expeditionary operations.

IDIQ Structure and Why It Matters

Indefinite Delivery / Indefinite Quantity (IDIQ) contracts are long-term umbrella agreements the U.S. Government uses to place many individual orders, known as task orders, over a period of years without rebidding the entire requirement each time.

Key points about IDIQs:

The IDIQ ceiling is the maximum total dollar amount that can be obligated across all task orders over the life of the contract.

The ceiling is not guaranteed revenue, but it defines the size of the addressable opportunity under that vehicle.

The base IDIQ award often carries little or no funding; meaningful dollars arrive through competitively awarded task orders inside the vehicle.

Holders of IDIQ positions gain ongoing opportunities to bid on task orders and capture work over the contract’s full term.

Across the federal market, particularly in the Department of Defense, a majority of contract spending now flows through IDIQ-type vehicles and other indefinite-delivery structures. Agencies are consolidating key mission areas into fewer, larger, multi‑award IDIQs with performance periods of 5–10 years or more and ceilings in the tens to hundreds of billions of dollars.

Within this environment, simply being “on the vehicle” with the right capability and capital structure is a significant strategic advantage.

Navy Counter Narcotics and Global Threats (CNGT) IDIQ

Under the U.S. Navy Counter Narcotics and Global Threats (CNGT) IDIQ:

Native American Pride Constructors participates in a vehicle with an approximate $1.9 billion maximum ceiling that runs into the 2032 timeframe.

The contract supports global counter‑narcotics and security missions, including:

Logistics and transportation support.

Training, advisory, and capacity-building activities.

Infrastructure and facilities-related work.

Operational support for U.S. forces and partner nations combating drug trafficking and associated threats.

NAPC Defense is designated as the primary subcontractor and principal public-company platform through which Native American Pride Constructors channels the majority of subcontracted work and associated revenues under this Navy IDIQ. This gives NAPC Defense a front-line role in an active, mission-focused portfolio of work with long-term duration and global scope.

Air Force Worldwide Expeditionary Multiple Award Contract (WEXMAC) IDIQ

Under the U.S. Air Force WEXMAC IDIQ:

Native American Pride Constructors holds a position on a multi‑prime vehicle with an approximate $55.2 billion ceiling that runs into the 2034 timeframe.

The vehicle supports worldwide expeditionary and base-support missions, including:

Logistics and sustainment operations.

Construction, engineering, and infrastructure projects.

Maintenance and facilities support.

Mission‑support services in base and operational theaters, including difficult and high‑risk environments.

NAPC Defense serves as the sole primary subcontractor platform through which Native American Pride Constructors routes the bulk of subcontracted work tied to this contract line. This structure creates a direct path for NAPC Defense to compete for and perform large, multi‑year task orders associated with one of the Air Force’s most significant expeditionary-support vehicles.

Specific Contract Transfer and Successor Status

The contract transfer is concrete. For example, Contract No. FA4890‑23‑D‑0008 is one of the Obera contracts transferred under this framework. Effective March 16, 2026:

Obera LLC transferred to Native American Pride Constructors all assets related to the performance of Contract No. FA4890‑23‑D‑0008 and other U.S. Government contracts.

Native American Pride Constructors assumed all obligations, duties, liabilities, and responsibilities under that contract.

Native American Pride Constructors became the lawful successor in interest under the United States Government’s FAR Subpart 42.12 novation procedures.

In connection with this, contracting officers also accepted NAPC Defense as the primary subcontractor responsible for executing the bulk of subcontracted work, confirming that the Government regards NAPC Defense as an appropriate main executor on these contracts.

Integrated Personnel and Execution Capability

The platform’s strength rests not only on contractual rights, but also on continuity of people and capabilities. As part of the Obera acquisition and transition:

Ten essential Obera employees were taken on within the combined structure.

This preserved critical institutional knowledge, customer relationships, program history, proposal capabilities, and field-execution expertise.

It ensured continuity for existing task orders and enhanced the platform’s ability to bid, win, and perform additional task orders in new areas.

When combined with Native American Pride Constructors’ construction and field-execution background and NAPC Defense’s management and operational teams, this personnel integration gives the platform a robust execution foundation.

Credit Line and Current Financial Activity

To support ongoing contract operations and scaling:

A new $20 million credit line has been agreed to for the platform performance.

This facility provides working capital for:

Procurement and supply-chain commitments for called on performance.

Subcontractor and vendor support.

General execution and growth under existing and new task orders.

In addition, management reports that contract payments received this month (April 2026) already exceed the $1 million mark, demonstrating that the platform has moved from a purely “pipeline” narrative into active contract execution with real cash inflows.

Additional Contract Pursuits

Beyond the existing backlog, NAPC Defense and Native American Pride Constructors are actively expanding the opportunity set:

The team is currently bidding on approximately $50 million in additional contracts under the existing IDIQ vehicles and related channels.

The strategy is to continuously pursue new task orders as the Government releases opportunities, leveraging the IDIQ positions, integrated personnel, and new credit facility.

This creates a dynamic pipeline layered on top of the $38.1 million hard backlog and the approximately $57.1 billion in combined IDIQ ceilings.

CornerShot Platform and Global Defense-Product Strategy

In parallel with its services and contracting platform, NAPC Defense has a differentiated product-based growth engine centered on the CornerShot system and associated munitions and weapons activities.

Key CornerShot Elements:

NAPC Defense holds exclusive licensing, production, and sales rights for CornerShot and related Scorpion technology in the United States and Middle East, as well as specified additional territories under its agreement with Silver Shadow of Israel.

The company is actively pursuing multiple sales opportunities for CornerShot with law-enforcement agencies, tactical teams, and specialized units in the U.S., multiple middle eastern countries and other approved allied markets.

Efforts include outreach to law-enforcement organizations, SWAT teams, school resource officer communities, and international security forces, with multiple channels being developed for domestic and international deployment.

Preparation for U.S. production of CornerShot, including tooling, metalwork, and plastics at selected U.S. manufacturers, has been completed, and all CornerShot units are planned for manufacture in the United States at Florida-based facilities.

This positions CornerShot as a scalable, life‑saving tactical system that can serve both international military customers and domestic law-enforcement and security markets, providing NAPC Defense with a proprietary product line alongside its contract-services activity.

CORNERSHOT TACTICAL SYSTEMS MARKET EXPANSION

International Middle East Platform Sales:

NAPC is pursuing Middle East defense ministry contracts for CornerShot tactical rifle and grenade launcher systems. The modeled volume across negotiated customers totals 40,000 systems generating $400 million in revenue calculated over a four year sales period. The NAPC cost per unit is $4,000, leaving flexibility in certain pricing situations.

Contribution margins vary by execution scenario: a conservative margin of 28% on $400,000,000 in gross CornerShot international sales yields a $112,000,000 contribution; a base‑case margin of 42% yields a $168,000,000 contribution; and an upside margin of 51% yields a $204,000,000 contribution.

Domestic United States Market:

NAPC Defense has developed a comprehensive domestic marketing strategy focused on school resource officers, law enforcement entities at local, county and Federal levels, as well as school districts, and related constituencies. The Company has established direct access to over 100,000 schools and 35,000 law enforcement agencies across the United States through marketing partnerships, convention participation, and outreach programs reaching parent groups and school boards. NAPC is on the cusp of large-scale acceptance through grants and other funding mechanisms for local agencies.

Broader Defense, Munitions, and Protection Capabilities

Beyond CornerShot, NAPC Defense’s broader capabilities include:

- Munitions and Technology Brokering

Sourcing and brokering of small arms and larger-caliber munitions for U.S. and allied forces under appropriate U.S. approvals.

Access to global inventory and manufacturing, allowing rapid response to approved demand.

- Firearms and Tactical Technologies

Suppressor development and specialized firearms-platform engineering for tactical use.

A range of weapons-related technologies designed for military and law-enforcement applications.

- Ballistic Protection and Armored Solutions

Ballistic-protection products (helmets, body armor, shields) via strategic partnerships.

Armored-vehicle sourcing and brokering for law enforcement, military, and select civilian security applications.

These lines provide a second growth engine that complements the government-contract platform, allowing NAPC Defense to participate in both services and equipment demand.

Native American Pride Constructors and Construction-Backed Mission Support

Native American Pride Constructors brings construction and infrastructure-focused capabilities that integrate directly with the current contract portfolio:

Experience in military and government construction and infrastructure projects.

Ability to support facilities, infrastructure, disaster-resilient construction, and mission-support requirements embedded in expeditionary and base-support contracts.

Direct alignment with the construction, engineering, sustainment, and mission-support components of WEXMAC and related vehicles.

Together with Obera’s legacy competencies in logistics, training, communications, fuels management, procurement support, supply-chain operations, facilities support, and work in austere environments, the combined platform is well positioned to deliver a full spectrum of services required by the Navy CNGT and Air Force WEXMAC IDIQs.

Market Environment and Strategic Position

These developments occur against a backdrop of sustained high defense spending in the United States and rising global military expenditure. This environment supports continued demand for:

Logistics, sustainment, and mission support.

Construction and infrastructure for defense facilities.

Tactical and weapons systems, including CornerShot.

Munitions, protective equipment, and armored solutions.

Training, advisory, and capacity-building support for U.S. and allied forces.

Within that context, NAPC Defense should now be understood as:

A government-approved primary subcontractor and public execution platform tied to an approved successor prime contractor holding major Navy and Air Force IDIQ positions.

A company with $38.1 million in hard backlog, approximately $57.1 billion in IDIQ ceiling access, an active $50 million bid pipeline, and a new $20 million credit line supporting operations.

An operator with integrated Obera personnel, construction-backed capability from Native American Pride Constructors, more than $1 million in current-month contract payments, and a proprietary CornerShot and munitions product platform targeting both international and domestic law-enforcement and defense markets.

Taken together, these elements support the conclusion that NAPC Defense has already moved beyond a purely developmental story and now operates as an active, multi-channel defense platform with real government-contract access, execution capability, capital support, current cash inflows, and multiple avenues for continued growth in both contracting and product markets.

PROFITABILITY PER SHARE IS BEING WORKED ON

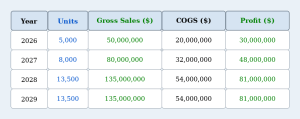

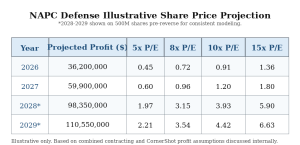

The combined contracting and CornerShot economics you’ve outlined support a reasonable illustrative share‑price projection path once you layer in 10% contracting margins, CornerShot profits, changing share count, and valuation multiples. Using your inputs, total modeled revenue across defense contracting plus CornerShot (international and domestic) comes out to roughly $120M in 2026, $195M in 2027, $297.5M in 2028, and $337.5M in 2029, with corresponding total net profit of about $36.2M, $59.9M, $98.35M, and $110.55M on a base-case margin set (10% on contracting and the CornerShot contribution figures used in your earlier planning.

2026 is a transition year where defense‑contract execution and initial CornerShot deployments combine into roughly $36M of profit on about $120M in revenue, against 400M fully diluted shares. Applying P/E multiples of 5x, 8x, 10x, and 15x to that profit would imply 2026 share‑price ranges of approximately $0.45, $0.72, $0.90, and $1.35 per share, respectively, which you can present as low, conservative, base, and high planning anchors rather than guidance.

In 2027, with contracting revenue stepping up to about $80M, international CornerShot moving further into its four‑year ramp, and domestic CornerShot adding a second growth leg, the combined model yields on the order of $195M revenue and $59.9M profit before the reverse split and before any additional dilution beyond the 500M‑share planning number. On that basis, the same 5x, 8x, 10x, and 15x multiples would correspond to implied pre‑reverse prices of roughly $0.60, $0.96, $1.20, and $1.80 per share at the 500M share level, which you can then translate to post‑reverse levels by multiplying by 10 once you describe the 10‑for‑1 consolidation.

For 2028, after the intended reverse split and assuming the share count is stabilized at an effective 50M economic equivalent (your planning grid treats 500M shares but you can present everything on a “post‑split” basis at one‑tenth the count), the same model delivers approximately $297.5M of revenue and $98.35M of profit as CornerShot’s four‑year program enters its heaviest years and contracting revenue reaches $100M. Using your 5x, 8x, 10x, and 15x P/E band, this leads to illustrative implied post‑split prices in the neighborhood of $9.80, $15.70, $19.70, and $29.50 per share, again framed as execution‑dependent, not as promises.

By 2029, with contracting revenue modeled at $120M and CornerShot’s international and domestic lines still contributing at strong margins, total revenue moves toward $337.5M with profit in the $110M range. At that point, the same multiple framework suggests potential post‑split price illustrations on the order of $11.00, $17.60, $22.10, and $33.20 per share, which can be shown in a simple four‑column table (Year, Profit, P/E, Implied Price) to demonstrate how improved operating scale plus a normalized small‑cap defense multiple combine to generate appreciation from a sub‑dollar 2026 base into mid‑ to high‑single‑digit or low‑double‑digit values.

IMPORTANT DISCLOSURES & FORWARD-LOOKING STATEMENTS

The Vanderbilt Report, an investor relations and financial communications publication, publishes this report. This report is for informational purposes only and does not constitute an offer to sell, a solicitation of an offer to buy, or a recommendation of any security. All content is derived from publicly available sources, including company press releases, SEC filings, and publicly available market research.

This report contains forward-looking statements. Actual results may differ materially from those projected or implied. Past performance is not indicative of future results. Investing in small-cap and micro-cap securities involves substantial risk, including the possible loss of principal. Readers are strongly encouraged to conduct their own due diligence and consult a licensed financial advisor before making any investment decision.