THE VANDERBILT REPORT

ADVANCED MATERIALS | EMERGING MARKETS | INSTITUTIONAL ANALYSIS

JUNE 2026

The Material That Keeps Almost Arriving

Graphene has promised to reshape industry for two decades. The production problem is finally being solved and a new class of operators is positioning to capture the transition.

The history of graphene is a study in earned patience. Discovered at the University of Manchester in 2004, isolated by Andre Geim and Konstantin Novoselov in work that earned a Nobel Prize six years later, graphene entered the public imagination as a material that would rewrite the physics of the modern world. One atom thick. Two hundred times stronger than steel. Electrical conductivity that surpasses copper. Thermal performance that eclipses diamond. The superlatives were accurate and they remain accurate. The question was never the science. It was the manufacturing.

Two decades on, that manufacturing question is being answered. The global graphene market, valued at roughly $340 million in 2025, is projected by multiple research institutions to reach between $4 billion and $16 billion by the early 2030s a trajectory that reflects not speculative enthusiasm but documented production progress. Capital is accelerating: over $185 million in disclosed funding entered the sector in 2025 alone, with production facilities now being commissioned across three continents. For the first time in the material's commercial history, the conversation has moved decisively past whether graphene works. The industry is now executing on how to deliver it at scale.

The answer is yes and the companies best positioned to capture that transition are the ones building quietly, with discipline, in sectors the market has not yet repriced.

THE PRODUCTION PROBLEM

Understanding graphene's commercial delay requires understanding its structural paradox. The properties that make graphene exceptional atomic-scale thinness, perfect lattice arrangement, zero defect tolerance are precisely the properties that make it extraordinarily difficult to manufacture consistently. Chemical vapor deposition, the dominant high-quality production method, requires temperatures above 1,000 degrees Celsius and produces graphene in quantities measured in square centimeters, not industrial volumes. Liquid-phase exfoliation, which can produce larger quantities, introduces defects that degrade the material's performance. The gap between laboratory graphene and commercial graphene has, until recently, been measured in orders of magnitude.

The early commercial wave reflected this reality. Initial graphene-enhanced products tennis rackets, cycling helmets, specialty coatings demonstrated that the material could be incorporated into manufactured goods at modest volumes. But the industrial applications that justified the material's long-term valuation required a different order of production capability. The construction sector, positioned to benefit from graphene-enhanced concrete capable of extending infrastructure lifespans by decades, needed consistent supply at industrial volumes. Agriculture needed reliable, cost-effective feedstocks. Energy storage required performance-grade graphene that could compete on total cost of ownership against incumbent battery chemistries. Each application was technically validated. The constraint was always production.

|

MARKET CONTEXT Nearly 33% of end users cite large-volume production scaling as their primary near-term challenge. Around 37% are actively investing in supply chain infrastructure for high-quality material. The production build-out is underway and the companies that have advanced furthest on this dimension hold the strongest commercial positions in the market. |

What changed in the last three years is not the physics the physics were always correct. What changed is process engineering: the capital-intensive, methodical work of developing production platforms that can reproduce consistent quality at meaningful throughput. Several companies have made material advances in this domain, and the cumulative effect is now visible in investment flows, commissioned capacity, and the first commercially deployed graphene-enhanced industrial products performing at specification in the field.

|

|

The physics of graphene have been established for two decades. What is being established now is the production architecture and with it, the commercial moment that the science always made possible. |

|

WHY THE TIMING MATTERS NOW

Several structural forces have converged to make 2025 and 2026 qualitatively different from any prior period in graphene's commercial history.

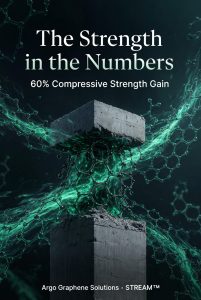

The first is infrastructure demand. The global construction sector faces mounting pressure to extend asset lifespans against strained public budgets and aging inventory. Graphene-enhanced concrete additives which research has shown can increase compressive strength meaningfully while reducing cement content address a specific, measurable problem that owners and contractors already understand and actively seek to solve. The value proposition requires no market education. It requires only a material substitution that delivers documented performance.

The second is agricultural transformation. Precision agriculture, already accelerating through adoption of GPS-guided equipment and soil sensor networks, is creating demand for materials that can enhance input efficiency. Graphene's properties as a soil amendment improving nutrient absorption and water retention fit within an existing commercial framework that farmers and distributors already operate within.

The third is energy storage urgency. The buildout of grid-scale storage required to support renewable energy penetration is creating sustained demand for battery technologies that outperform incumbent lithium-ion chemistries on cycle life and charge speed. Graphene-enhanced electrodes have demonstrated performance advantages in controlled environments, and the production platforms now reaching commercial scale are delivering those advantages in manufactured products at competitive cost structures.

Each of these applications shares a critical characteristic: the commercial case does not rest on graphene being exceptional. It rests on graphene being reliably better and reliably available.

Investment capital has recognized the shift. The $55 million Series C secured by Paragraf in 2025 the largest single funding round in the sector's history was not a bet on graphene's properties. Those have been established for twenty years. It was a bet on Paragraf's ability to manufacture wafer-scale graphene electronics with the consistency required for commercial semiconductor applications. The distinction matters. Capital is no longer funding the science. It is funding the factory.

WHAT THE MARKET IS MISSING

The opportunity in graphene has always been visible. What is becoming clearer and what the market is beginning to price is exactly where value accrues. The companies that will define graphene's commercial era are not those with the broadest application ambitions. They are those with defensible production platforms: proprietary processes for manufacturing consistent graphene at controlled cost structures, paired with the commercial discipline to sequence market entry rather than pursuing every vertical simultaneously.

This is the analytical distinction that separates the current wave of graphene operators from their predecessors. The sector's early years produced excellent science and premature commercialization. What the field has learned and what its best operators have internalized is that production credibility must precede distribution ambition. The companies that have solved production first, and built their commercial frameworks around that sequence, are the ones advancing toward durable market positions.

|

STRUCTURAL OBSERVATION The graphene sector's commercial inflection is defined by a single variable: production platform maturity. Companies that have achieved consistent, certifiable output at commercial volumes now hold the strongest positions the sector has ever seen. The market is beginning to recognize this distinction and reprice accordingly. |

The opportunity is not being missed it is being sequenced. The investors who follow that sequence, rather than the headlines, will find the most durable positions.

THE OPERATOR QUESTION

The transition from development-stage to commercially operating graphene company is the most consequential threshold in the sector and the most revealing one. Production platforms that perform at laboratory scale must be engineered for ten tons per annum. Supply chain relationships adequate at pilot scale must be formalized into durable commercial agreements. Capital discipline must become structural. The operators who navigate this transition successfully have one thing in common: they built accountability into their technology acquisition deals before capital was deployed, not after. Deal structure, in advanced materials, is where operator conviction becomes visible.

What separates the operators positioned to succeed is not technology alone it is deal architecture. The most sophisticated actors in the current wave of graphene commercialization have structured their technology acquisitions and partnerships to tie capital deployment to demonstrated execution milestones. Equity is earned, not given upfront. Licensing converts to ownership upon commercial validation. Inventors and technology holders are incentivized through governance stakes rather than cash buyouts that extract them from the outcome.

This architecture serves multiple functions simultaneously. It conserves capital during the highest-uncertainty phase of development. It aligns incentive structures across technology providers, operators, and investors. And it creates verifiable external validation points commissioned facilities, independent certification, revenue thresholds that distinguish genuine progress from promotional narrative.

CASE STUDY: ARGO GRAPHENE SOLUTIONS CORP. (CSE: ARGO | OTCQB: ARLSF)

The principles above are visible in practice in the structure recently executed by Argo Graphene Solutions Corp., a Canadian advanced materials company that closed a license and technology transfer agreement with Grapherry, Inc. in June 2026 covering Grapherry's proprietary STREAM graphene production platform.

The deal is notable not primarily for its subject matter graphene licensing transactions have occurred with regularity but for its construction. The agreement grants Argo an exclusive worldwide license to use, develop, manufacture, and commercialize the STREAM technology. Full ownership of the platform transfers automatically upon the issuance of all consideration equity. That equity, totaling up to 11 million common shares and 5.5 million warrants, is structured almost entirely around performance milestones rather than issued on closing.

The milestone structure is precise: 2.5 million shares vest upon completion of a CAD $1 million equity financing; 3 million upon commissioning of a graphene production facility meeting minimum capacity specifications as confirmed by an independent third party; and 3 million upon achieving CAD $1 million in gross revenue from commercialization. Each threshold represents a distinct operational gate capital availability, production validation, and commercial proof in the sequence that actually governs whether a development-stage materials company becomes a commercial one.

This is not standard deal architecture for a junior Canadian materials issuer. It reflects an operator that understands where advanced materials companies fail and has built accountability into the transaction at precisely those points.

The governance dimension of the agreement reinforces the structural read. Vikas Berry, CEO of Grapherry and the architect of the STREAM platform, has been appointed to the board of directors of Argo. His equity tied to the same milestones as the license creates direct alignment between the technology originator and the commercial outcome. He is not cashing out. He is staying in.

Argo's focus applications graphene-enhanced concrete and cement additives, infrastructure materials, agricultural applications, and specialty industrial products map directly onto the market verticals where production consistency translates most rapidly into commercial value. These are not frontier applications requiring market education. They are established industries with existing procurement frameworks and a demonstrated willingness to adopt materials that reduce costs or extend asset life.

Argo is executing the right sequence at the right time. The path from licensing agreement to commissioned facility to first commercial revenue is well-defined. The milestone structure capital raise, independent production certification, revenue validation creates a transparent set of markers against which progress is measured and ownership is earned. Each milestone achieved expands the company's operational foundation and validates the next phase. The design of the deal anticipates execution, not just aspiration.

|

WHAT INVESTORS SHOULD WATCH The critical validation signal is the independent third-party commissioning certification of the production facility. This milestone not the equity financing and not initial revenue is the operational gate that most directly predicts whether Argo transitions from licensing structure to commercial platform. Watch for the timeline and technical specifications announced for that facility. |

THE STRUCTURAL CONCLUSION

Graphene's commercialization arc has been long, and the patience it required was real. But the discipline of that development period produced something valuable: a production foundation built on validated science rather than promotional expectation. The operators now advancing toward commercial scale are doing so with proof-of-performance assets, milestone-structured capital deployment, and application focus in sectors where the value proposition is already understood by buyers.

The sector's inflection point is not a single product launch or a single application breakthrough. It is the systematic maturation of production platforms capable of delivering consistent material quality at commercial volumes a capability that is now being demonstrated, documented, and certified by independent parties. The market data reflects the shift. The investment flows confirm it. The deal structures being executed now reveal exactly where sophisticated operators believe the commercial opportunity is concentrated.

The transformation graphene was always capable of delivering is now being built into commercial reality by operators who structured their deals to prove it, not just promise it.

Argo Graphene Solutions is a direct expression of that discipline. Its STREAM-based production platform, milestone-anchored deal structure, and application focus in construction, infrastructure, and agriculture position it at the intersection of the market's strongest near-term demand vectors. The company is executing the right sequence, in the right sectors, with incentive structures that keep the people who built the technology invested in seeing it succeed.

The material has earned its commercial moment. The operators building toward it are the ones worth watching.

2026 The Vanderbilt Report. All rights reserved.