Executive Summary

Jaguar Health, Inc. (NASDAQ: JAGX) represents a unique investment opportunity in the specialty pharmaceutical sector, combining FDA-approved products with a robust pipeline targeting high-value orphan disease markets. With strong revenue growth momentum, breakthrough clinical data, and multiple near-term regulatory catalysts, the company is positioned to deliver substantial returns for forward-thinking investors.

Vanderbiltreport Investment Opportunity

Business Overview

Jaguar Health, Inc. (NASDAQ: JAGX) is a pioneering commercial-stage pharmaceutical company focused on developing novel, plant-based, sustainably-derived prescription medicines for gastrointestinal distress in both humans and animals. The company’s unique value proposition centers on crofelemer, the only oral FDA-approved prescription drug under botanical guidance, extracted from the Croton lechleri tree in the Amazon Rainforest.

Call your Broker now!

November 19, 2025

Core Business Segments

Human Health Division:

The company’s flagship product, Mytesi (crofelemer 125mg delayed-release tablets), is FDA-approved for the symptomatic relief of non-infectious diarrhea in adults with HIV/AIDS on antiretroviral therapy. This first-in-class anti-secretory agent operates through a unique mechanism of action that normalizes gut function without the drawbacks of traditional opioid-based treatments.

Animal Health Division:

Through its Jaguar Animal Health tradename, the company markets Canalevia-CA1, which received conditional FDA approval for chemotherapy-induced diarrhea in dogs. This addresses a significant unmet need in veterinary oncology, with an estimated 11 million dogs suffering from general diarrhea annually in the U.S. alone.

Sustainable Sourcing & ESG Commitment

Jaguar has established a comprehensive sustainable harvesting program for crofelemer under fair trade practices, ensuring ecological integrity and supporting indigenous communities in South America. This commitment to environmental stewardship and social responsibility positions the company favorably with ESG-focused investors while securing long-term supply chain stability.

Market Analysis

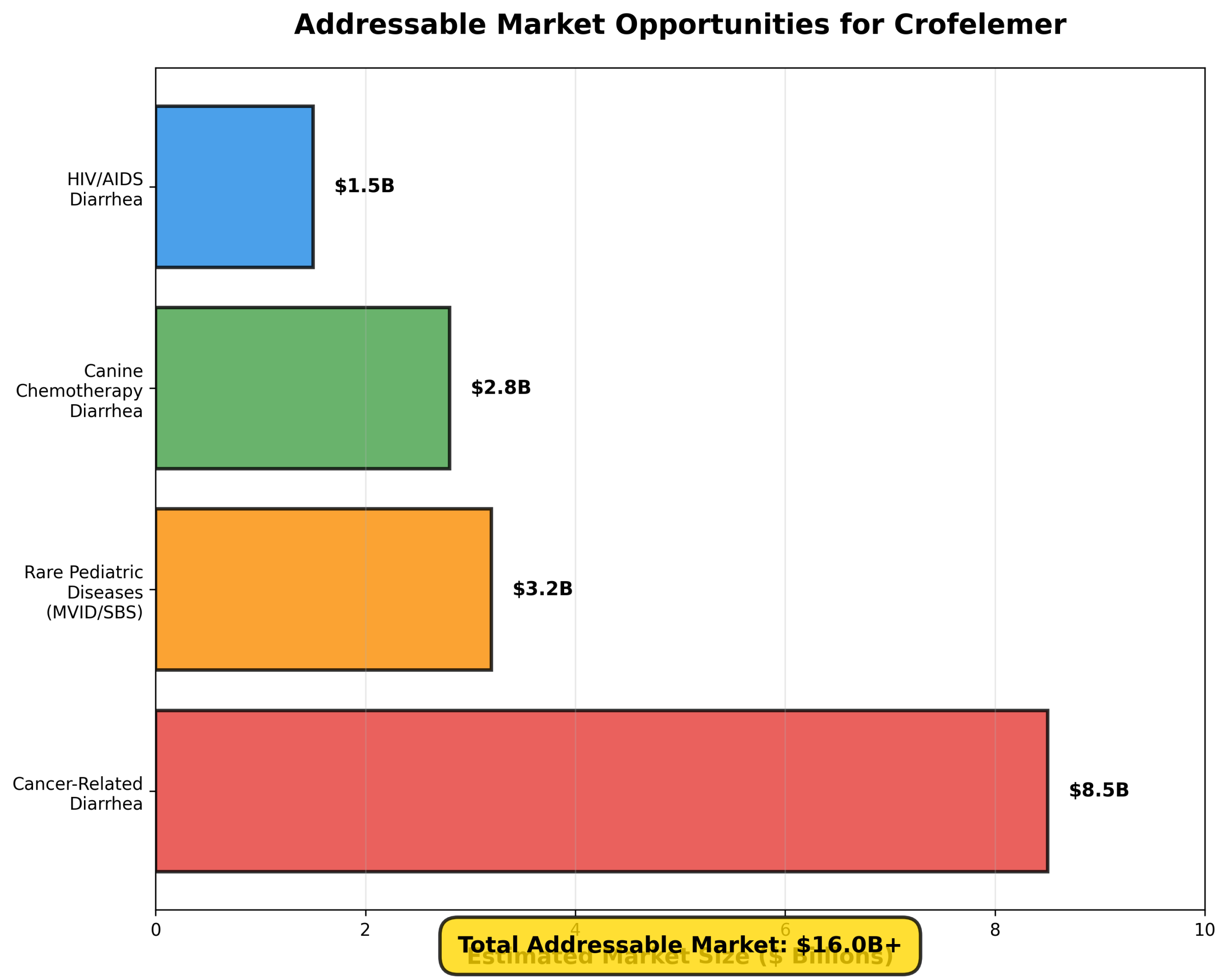

Massive Addressable Markets

Jaguar Health operates at the intersection of several high-growth pharmaceutical markets, each representing billions of dollars in potential revenue:

Figure 1: Estimated addressable market opportunities across Jaguar’s therapeutic focus areas

Don’t miss this opportunity

Cancer Therapy-Related Diarrhea (CTD)

The oncology supportive care market represents Jaguar’s largest opportunity. Cancer therapy-related diarrhea affects millions of patients annually, particularly those receiving targeted therapies and chemotherapy. The market for CTD treatments is estimated to exceed $8 billion globally, with limited effective treatment options currently available.

Breakthrough Results in Breast Cancer: Statistically significant responder analysis results from the Phase 3 OnTarget trial in breast cancer patients have positioned crofelemer for potential breakthrough therapy designation from the FDA. With metastatic breast cancer patients qualifying as an orphan population in the U.S., Jaguar can pursue expedited regulatory pathways while benefiting from market exclusivity protections.

Rare Pediatric Diseases – Orphan Drug Advantages

Jaguar’s strategic focus on ultra-rare pediatric intestinal failure diseases offers compelling commercial advantages:

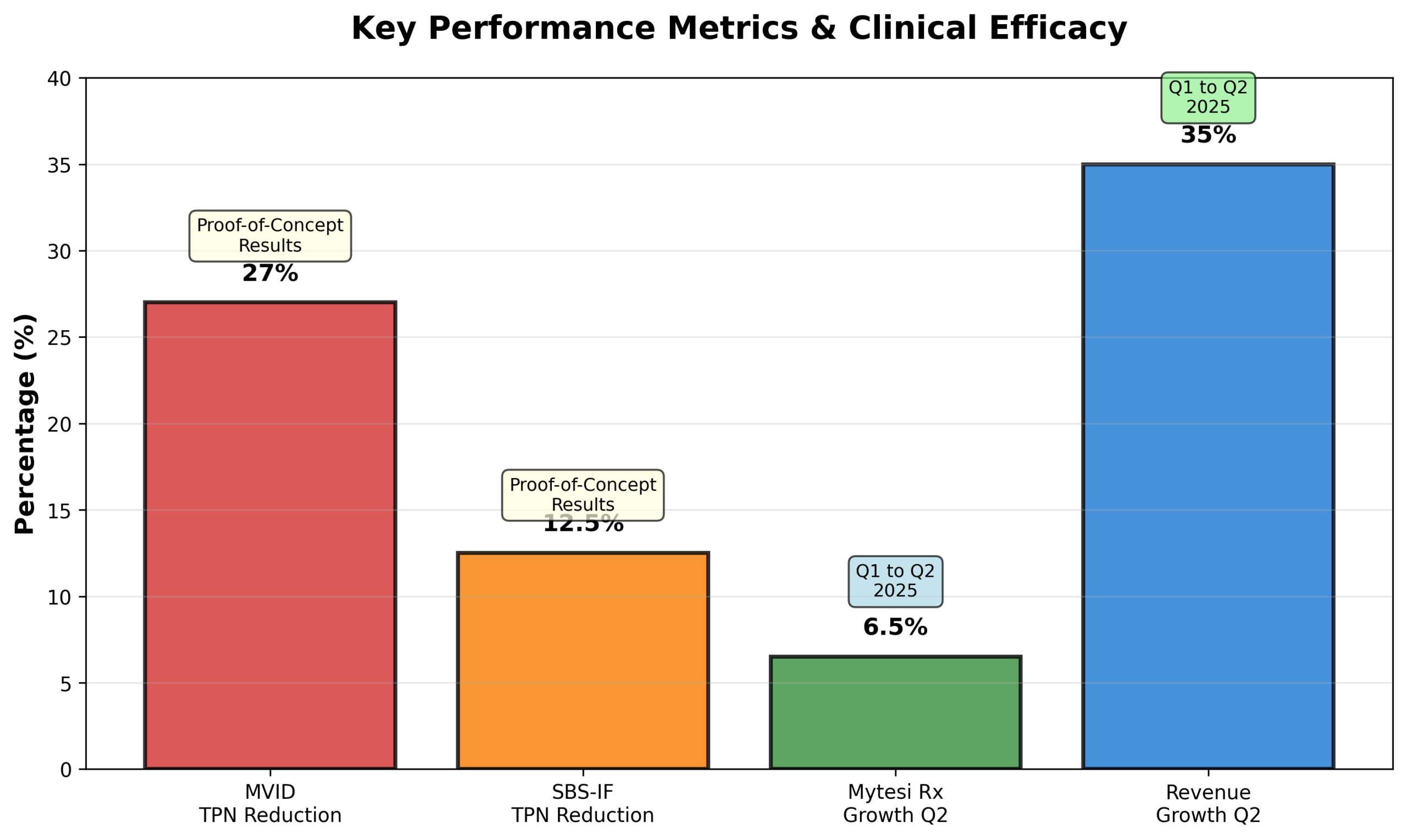

- Microvillus Inclusion Disease (MVID): With only 100-200 patients worldwide, this devastating congenital disorder has no approved treatments. Proof-of-concept data showing up to 27% reduction in total parenteral nutrition requirements represents a paradigm-shifting therapeutic advance.

- Short Bowel Syndrome with Intestinal Failure (SBS-IF): Affecting 10,000-20,000 patients in the U.S. and Europe, this market offers substantial revenue potential with orphan drug pricing and seven-year market exclusivity.

- Regulatory Incentives: Orphan drug designation provides tax credits for clinical development, exemption from FDA filing fees, and potential access to priority review vouchers that can generate immediate value through sale (historically valued at $80-350 million).

Veterinary Oncology – Underserved Market

The companion animal health market continues to experience robust growth, driven by increasing pet ownership and willingness to invest in advanced veterinary care. With an estimated 30 million U.S. dog owners having experienced canine cancer, Canalevia-CA1 addresses a significant market gap as a non-antibiotic treatment option.

Competitive Analysis

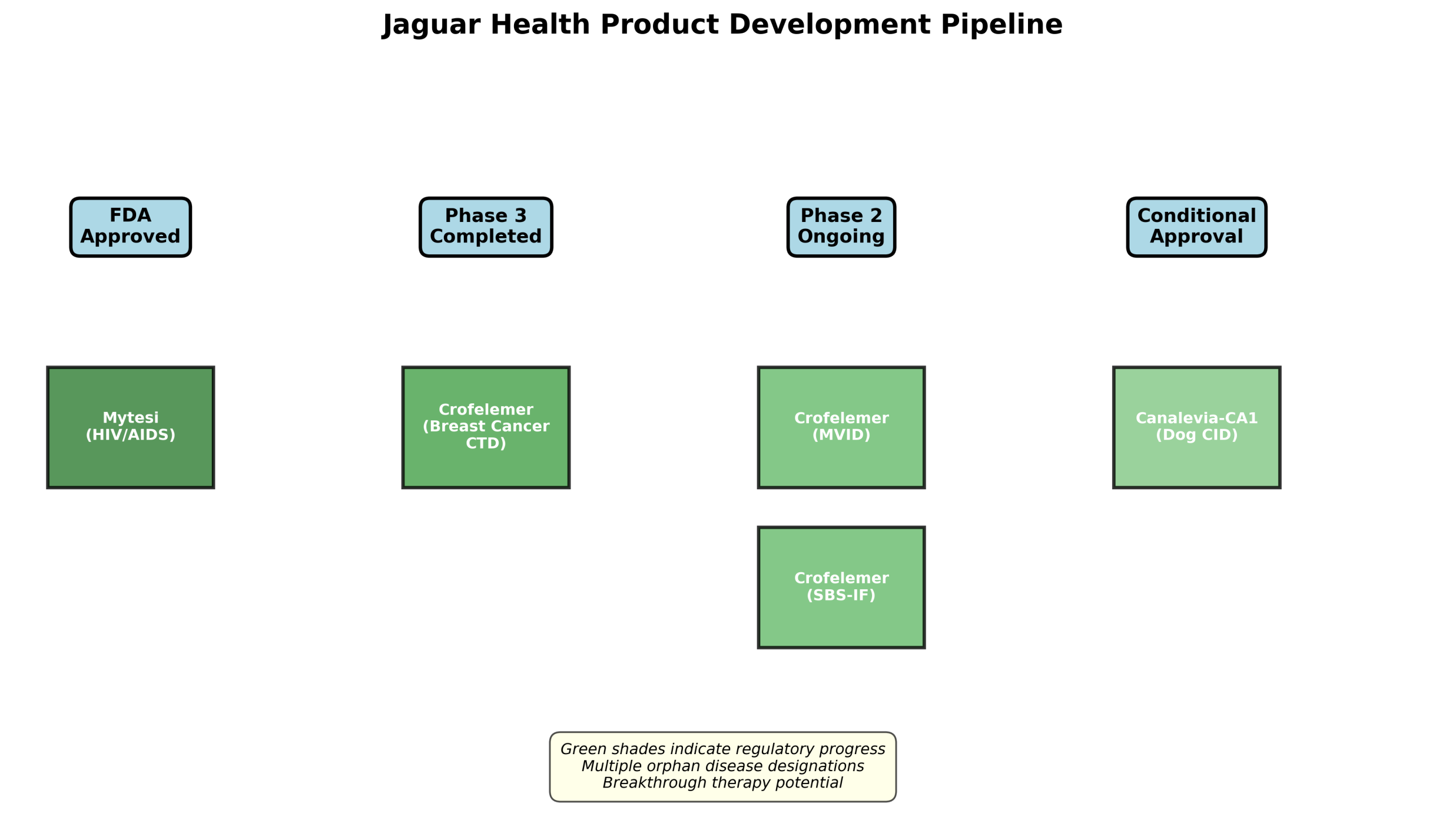

Unique Competitive Advantages

1. First-in-Class Mechanism of Action: Crofelemer’s plant-based, non-opioid mechanism represents a novel approach to treating secretory diarrhea. Unlike traditional anti-diarrheal medications that can cause constipation or carry addiction risk, crofelemer normalizes gut function without these drawbacks.

2. Botanical Drug Classification: As the only oral FDA-approved prescription drug under botanical guidance, Jaguar benefits from a unique regulatory position that combines rigorous pharmaceutical standards with streamlined development pathways for botanical products.

3. Multiple Orphan Designations: The company has secured orphan drug designation from both the FDA and European Medicines Agency (EMA) for MVID, SBS-IF, and cholera-related diarrhea, providing significant competitive protection and regulatory advantages.

4. Vertical Integration: Through family companies Napo Pharmaceuticals and Napo Therapeutics S.p.A., Jaguar maintains control over development, manufacturing, and commercialization, capturing value across the pharmaceutical value chain.

Figure 2: Jaguar Health’s diversified product development pipeline spanning multiple regulatory stages

Competitive Landscape

In the cancer supportive care market, Jaguar faces limited direct competition for prophylactic treatment of CTD. Current standards of care focus primarily on reactive treatments after diarrhea develops, whereas crofelemer’s prophylactic approach addresses an unmet need for prevention.

For rare pediatric diseases, the ultra-orphan nature of MVID means virtually no competing therapies exist. In SBS-IF, while some treatments target nutritional absorption, none address the fundamental secretory mechanisms that crofelemer modulates.

Buy Now

Financial Analysis & Projections

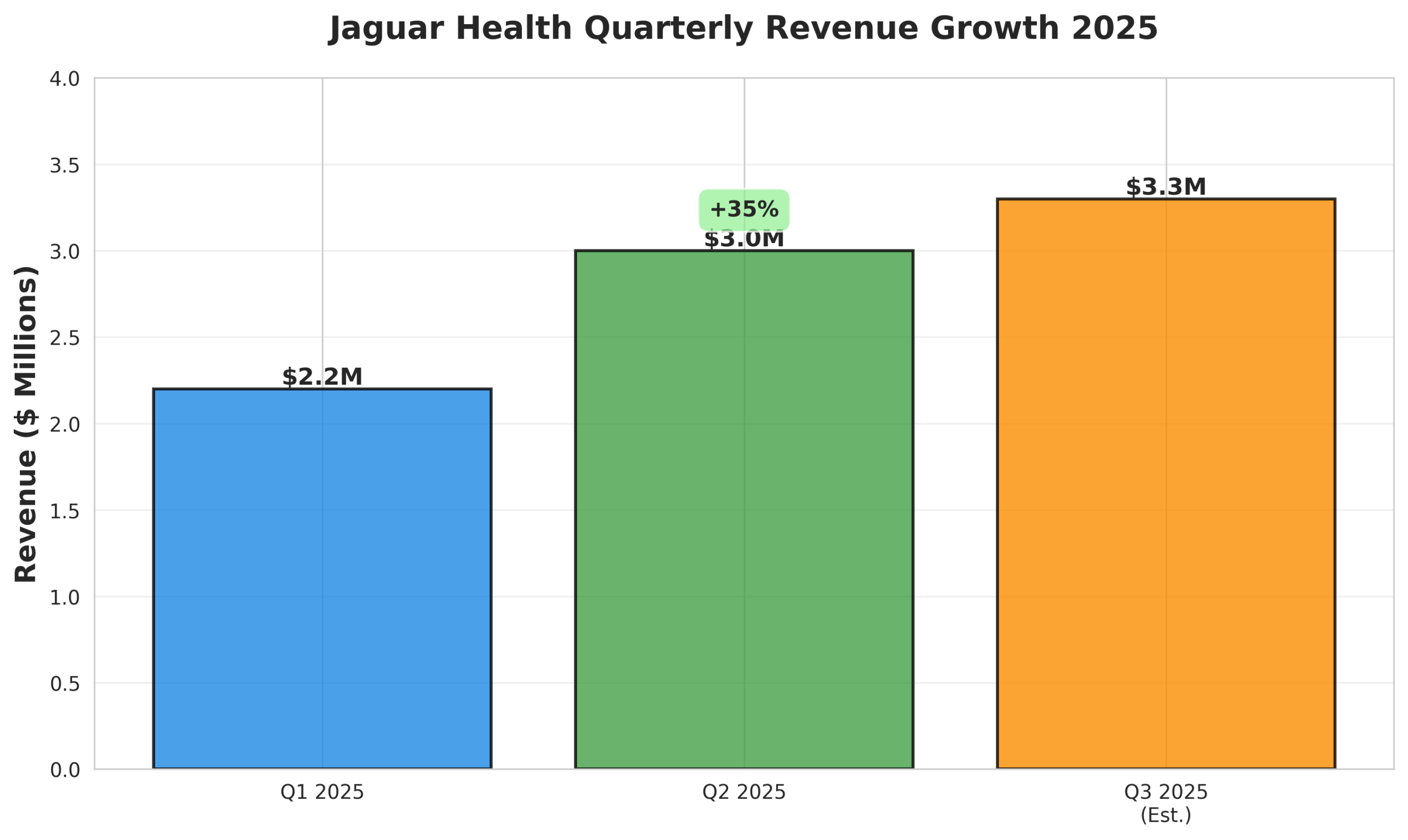

Strong Revenue Growth Trajectory

Q2 2025 Revenue: $3.0M (+35% vs Q1 2025)

2024 Annual Revenue: $11.7M (+20% vs 2023)

Mytesi Growth: +6.5% Q2 Prescription Volume

Analyst Price Target: $14.17 (Strong Buy Rating)

Figure 3: Quarterly revenue progression demonstrating accelerating growth momentum

Financial Performance Highlights

- Revenue Acceleration: The 35% quarter-over-quarter revenue increase in Q2 2025 demonstrates strong commercial traction for Mytesi and validation of the company’s market strategy.

- Improving Operational Efficiency: Non-GAAP recurring EBITDA loss improved to $7.9 million in Q2 2025 from $8.8 million in Q2 2024, showing progress toward profitability despite continued R&D investment.

- Strategic Capital Allocation: Recent securing of a $10.8 million note agreement and $1.5 million registered direct offering provides runway for critical clinical milestones while management actively pursues non-dilutive partnership arrangements.

Growth Projections & Value Creation

Near-Term Revenue Drivers (2025-2026):

- Continued Mytesi prescription volume growth in established HIV/AIDS market

- Potential approval and launch of crofelemer for metastatic breast cancer CTD

- Early access programs in Europe for MVID and SBS-IF generating initial revenues

- Canalevia expansion to general diarrhea indication in dogs.

Medium-Term Catalysts (2026-2028):

- Full commercialization of orphan indications with premium pricing ($100,000+ annually per patient for MVID/SBS-IF)

- Partnership deals providing upfront payments, milestones, and royalties

- Expansion into additional oncology indications beyond breast cancer

- International market penetration through Napo Therapeutics in Europe

- Potential sale of priority review voucher if obtained for cholera indication ($80-350 million value)

Valuation Perspective

With a current market capitalization of approximately $4-6 million and analyst price targets of $14-16 per share, Jaguar Health, Inc. (NASDAQ: JAGX) represents significant upside potential. Comparable orphan drug developers with similar pipeline depth typically command valuations in the $200-500 million range, suggesting current pricing offers an attractive entry point for investors willing to accept development-stage risk.

The company’s multiple shots on goal strategy—combining commercial products, late-stage trials, and multiple orphan programs—provides diversified value creation pathways that reduce binary outcome risk typical of single-asset biotechnology companies.

Clinical Validation & Key Catalysts

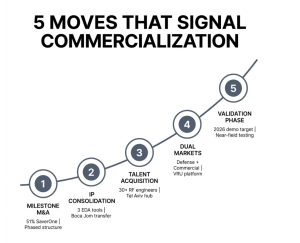

Figure 4: Key clinical and operational performance metrics demonstrating therapeutic efficacy and commercial momentum

Proof-of-Concept Success

Recent clinical data validates crofelemer’s therapeutic potential across multiple indications:

MVID Breakthrough: Initial results from the investigator-initiated trial in Abu Dhabi demonstrated up to 27% reduction in total parenteral nutrition requirements—a clinically meaningful improvement for patients dependent on IV feeding. This data supports potential Breakthrough Therapy designation from the FDA and inclusion in the EMA’s PRIME program for expedited regulatory approval.

SBS-IF Validation: Proof-of-concept data showing 12.5% reduction in parenteral support for short bowel syndrome patients provides evidence of crofelemer’s broad applicability in intestinal failure conditions, expanding the addressable market beyond MVID.

Breast Cancer CTD Results: Statistically significant results in the Phase 3 OnTarget trial’s prespecified breast cancer subgroup (183 of 287 participants) demonstrated efficacy in preventing cancer therapy-related diarrhea. The FDA’s granting of a Type C meeting to discuss these results signals regulatory receptivity to the data.

2025-2026 Catalyst Timeline

Q4 2025:

- Q3 2025 financial results (November 17, 2025)

- Presentation of MVID trial data at NASPGHAN Annual Meeting

- Continued enrollment in Phase 2 placebo-controlled studies

- Potential partnership announcements for orphan programs

Q1-Q2 2026:

- Submission of protocol to FDA for pivotal treatment trial in metastatic breast cancer

- Additional proof-of-concept results from multiple clinical sites

- Initiation of expanded access programs for breast cancer patients

- Potential Breakthrough Therapy or Fast Track designation applications

- European early access programs potentially generating revenue

H2 2026:

- Phase 2 placebo-controlled trial readouts for MVID

- Potential supplemental NDA filing for breast cancer indication

- Canalevia expansion to general diarrhea indication

- Potential partnership deal closings with upfront payments

Investment Highlights

Why Invest in Jaguar Health Now?

1. De-Risked Commercial Stage: Unlike pure development-stage biotechs, Jaguar already generates revenue from FDA-approved products, providing downside protection while maintaining substantial upside from pipeline development.

2. Multiple Value Inflection Points: With five ongoing clinical programs, numerous regulatory interactions, and partnership discussions, investors benefit from multiple near-term catalysts that could drive significant appreciation.

3. Orphan Drug Economics: The company’s focus on rare diseases offers premium pricing power, extended market exclusivity, and reduced competitive pressure—fundamentals that typically command higher valuations in the pharmaceutical sector.

4. Regulatory Tailwinds: FDA Commissioner Dr. Marty Makary’s April 2025 comments about opening new regulatory pathways focused on “plausible mechanism” for rare/incurable diseases align perfectly with Jaguar’s orphan-focused strategy and crofelemer’s novel mechanism of action.

5. Strategic Partnerships Potential: Management’s explicit strategy to license orphan indication programs to larger pharmaceutical partners could generate significant non-dilutive funding, validation of technology, and potential royalty streams without surrendering core commercial products.

6. Undervalued Entry Point: Current market capitalization significantly undervalues the company’s commercial assets and pipeline potential, with analyst consensus suggesting 500%+ upside to fair value.

Analyst Consensus

Rating: Strong Buy (6 analysts consensus)

Average Price Target: $14.17 per share

Current Trading Range: $1.78-$2.10 per share

Implied Upside: 575%+

Risk Factors & Considerations

⚠️ Important Investment Disclaimer: All investments carry risk, and microcap pharmaceutical companies involve heightened volatility and uncertainty. Investors should carefully consider the following risk factors and conduct thorough due diligence before making investment decisions.

Clinical & Regulatory Risks

- Trial Outcomes: Ongoing Phase 2 studies may not replicate proof-of-concept results, potentially delaying or preventing regulatory approval

- FDA Approval Uncertainty: Despite positive meetings and promising data, there is no guarantee the FDA will approve crofelemer for new indications

- Timeline Extensions: Clinical development frequently encounters delays due to enrollment challenges, data analysis, or regulatory feedback

Financial Risks

- Cash Runway: The company continues to generate losses and may require additional capital raises, potentially diluting existing shareholders

- Partnership Dependency: Inability to secure favorable partnership terms for orphan programs could impact development timelines and valuation

- Revenue Concentration: Current revenue heavily dependent on Mytesi sales in a limited patient population

Market & Competitive Risks

- Small Market Cap: The company’s microcap status ($4-6M) creates liquidity constraints and amplifies volatility

- Competition: Larger pharmaceutical companies may develop competing therapies with greater resources

- Reimbursement: Payer acceptance and reimbursement rates for new indications remain uncertain

Operational Risks

- Supply Chain: Dependence on sustainable harvesting from the Amazon rainforest creates unique sourcing risks

- Key Personnel: Success depends significantly on an experienced management team and scientific advisors

- NASDAQ Compliance: Historical challenges with NASDAQ listing requirements could impact trading

- Don’t miss this opportunity

Conclusion

Jaguar Health, Inc. (NASDAQ: JAGX) represents a compelling investment opportunity for investors seeking exposure to innovative pharmaceutical development with multiple value creation pathways. The company’s unique positioning at the intersection of commercial-stage products, breakthrough clinical data, and high-value orphan disease markets creates a diversified risk-reward profile rarely seen in microcap biotechnology.

The convergence of several favorable factors—accelerating revenue growth, validated clinical efficacy, supportive regulatory environment, and strategic partnership potential—suggests the current valuation significantly underprices the company’s prospects. With analyst price targets implying 500%+ upside and multiple near-term catalysts on the horizon, Jaguar Health merits serious consideration for portfolios seeking growth opportunities in specialty pharmaceuticals.

While the risks inherent in early-stage pharmaceutical development cannot be dismissed, Jaguar’s multiple shots on goal strategy, combined with already-commercialized products providing revenue support, offers a more balanced risk profile than typical development-stage biotechnology investments. For investors with appropriate risk tolerance and investment horizons, Jaguar Health presents an opportunity to participate in potentially transformative therapies while benefiting from the premium valuations typically accorded to orphan drug developers.

Investment Recommendation: Jaguar Health, Inc. (NASDAQ: JAGX) merits a STRONG BUY rating for growth-oriented investors. The combination of near-term catalysts, breakthrough clinical data, strategic orphan disease focus, and significant valuation disconnect creates an asymmetric risk-reward opportunity. Recommended position sizing should reflect individual risk tolerance, with the microcap nature of the security suggesting this as a high-conviction, high-risk allocation within a diversified portfolio.

DISCLAIMER

Vanderbiltreport.com is owned and operated by AB Holdings, a US-based corporation. We have received compensation of up to $100,000 regarding the profiling of Jaguar Health, Inc. (NASDAQ: JAGX) starting on Sept 1, 2025. It is important to note that we do not own any shares in JAGX: NASDAQ.

This page includes forward-looking statements subject to substantial risks and uncertainties. Actual outcomes may differ due to, regulatory decisions, financing needs, and execution. Investors should consult SEC filings before making decisions.