Brookmount Explorations (Brookmount Gold)

Company Profile & Strategy

Brookmount Explorations, Inc. (doing business as Brookmount Gold) is a U.S.-based gold exploration and production company founded in 2018.

The company’s vision is to acquire, develop, and produce high-quality gold assets in jurisdictions such as Indonesia and North America.

Key strategic pillars include:

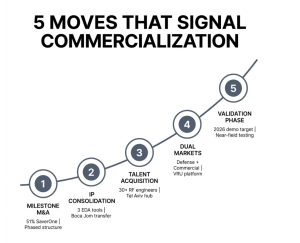

Production and cash flow generation

Portfolio expansion

Value plus shareholder-alignment moves

Uplisting ambition

Portfolio Highlights – Here are some of the key mining assets in Brookmount’s portfolio:

Indonesia – Talawan and Alason

According to the company website, Brookmount’s Indonesian operations include the Talawaan and Alason projects.

At the Talawaan operation, the company has reported very high ore grades (in one case, ~15 grams per tonne average from a single shaft) after taking full control of the operations.

These operations provide an existing production base and cash flow that Brookmount aims to leverage for growth and expansion.

North America – Moosehorn (Yukon, Canada), McArthur Creek (USA)

-

The Moosehorn Gold Project in the Yukon’s famed Tintina Gold Belt: The property spans ~4,300 hectares and carries an NI 43-101 complied resource estimate of 39,000 oz gold to date.

-

The McArthur Creek Project in Alaska is positioned on a 330-acre property with both placer and hard-rock gold deposits. Brookmount notes a “25-foot thick gold pay zone.”

These North American assets represent longer-term development opportunities that, if advanced, could add significant value to the company.

Recent Milestones & Financials

Brookmount has recently reached a number of noteworthy milestones:

-

Q1 2025 performance: The company reported revenue of approximately. US$3.4 million and a net profit of US$2.1 million for the quarter ending February 28, 2025.

-

Annual results for FY 2024: Filed March 17, 2025, the company reported revenue of US$18.45 million (up ~8.1 % from 2023’s US$17.06 million) and net income of US$9.18 million (EPS US$0.07) for the year ended November 30, 2024.

-

Stock buy-back authorization: The Board approved the repurchase of up to 10 million shares (maximum US$500,000) at up to US$0.05 per share. Shares repurchased are to be retired.

-

Convertible debt settlement/dilution controls: Brookmount announced an agreement to eliminate further stock conversions from its convertible debt and to reprice its Reg A offering to reduce dilution.

-

Website relaunch & IR portal: On October 21, 2025, Brookmount launched its revamped website (https://www.brookmountau.com) and investor relations portal, improving transparency and accessibility.

Growth Catalysts

Here are some of the catalysts that could drive future growth for Brookmount:

-

Uplisting to a senior exchange: Once audited financials and full reporting status are achieved, a move to a major exchange could boost liquidity, investor awareness, and valuation multiple.

-

North American asset spinoff/development: Reports suggest Brookmount is working toward a Q1 2026 spinoff of its North American assets into a separate company, which could unlock value by isolating different risk/return profiles.

-

Production ramp and ore-grade leverage: The Indonesian operations’ high grades (e.g., ~15 g/t) give the company a margin advantage. Scaling production from these assets could significantly boost cash flow.

-

Strategic acquisitions: The company’s acquisition of the Atlin Project in British Columbia (Canada), 70% interest, announced in April 2023, shows the appetite for growth in North America.

-

Share-buyback & dilution control: By reducing dilution (i.e., limiting new share issuance, eliminating convertible debt conversions), Brookmount is aligning with shareholder interests and support of the equity base.

Risks & Considerations

As with any junior mining company, particularly one trading on the OTC market, there are risks to be aware of:

-

Regulatory & audit risk: The company is still working to complete audits and achieve full reporting status. Delays or issues in this process could hamper uplisting efforts.

-

Operational risk: Mining is capital-intensive and subject to geological, technical, environmental, permitting, and cost‐overrun risks. Growth from North American projects remains in development.

-

Dilution risk: Although Brookmount is working to limit new share issuance, historically, junior miners often require additional financing, which may dilute existing shareholders.

-

Commodity risk: Gold prices fluctuate. While high-grade operations offer some margin buffer, external pricing remains an important variable.

-

Market liquidity / OTC status: As an OTC-listed company, liquidity and investor access are more limited than on senior exchanges. The transition to a better exchange is a potential benefit, but until then, the risk is higher.

-

Verification of resource claims: While there are NI 43-101 compliant estimates (e.g., Moosehorn at 39,000 oz) many assets are still in exploration or early development. Returns are not guaranteed.

Bottom Line

Brookmount Explorations (OTC: BMXI) presents an interesting potential opportunity in the junior gold mining sector with several positive attributes:

-

A producing operation in Indonesia with high ore grades and profit in recent quarters.

-

A growing pipeline of assets in North America, offering future upside.

-

Structural moves (buybacks, debt settlement, export to minimize dilution) that align with shareholder value creation.

-

Catalytic potential via uplisting and asset spinoff, which could re-rate the stock.

At the same time, key risks remain: execution risk, financing risk, commodity cyclicality, and the inherent risks of junior mining and OTC investing.

For investors with a higher risk tolerance, Brookmount could be worth further due diligence. For more conservative investors, the risk profile may warrant waiting until key milestones (e.g., senior exchange listing) are achieved.

Jake Rivers

submissions@vanderbiltreport.com

Compliance Note: